President Biden’s recent letter to refiners to complain of high gasoline prices is the only positive action he can take on behalf of consumers. But it won’t keep the average price at the pump in the U.S. from climbing another dollar by September and topping $6.

Here’s why: shrinking U.S. refining capacity even as oil

CL.1,

output recovers from COVID-19 pandemic lows, and a well-known shift in European demand away from Russia has cut into U.S. stockpiles more deeply than many realize. Plus Biden’s ability to act is further limited by underappreciated policy decisions that, ironically, he helped to make.

The first big policy shift occurred in 1973 – the year Biden joined the Senate — when President Nixon removed President Eisenhower’s oil import quota to fight inflation. OPEC’s cheap oil began to flood the U.S. market and undercut domestic producers.

The subsequent Arab oil embargo from October 1973 to March 1974 raised crude oil prices everywhere except the U.S., because Nixon’s August 1973 price controls were in force. While domestic refiners could buy foreign oil and refine it – which they did – selling it at home was a money-loser. The gasoline that did come the domestic market was limited by the amount of price-controlled domestic crude oil. That’s what led to long lines of people waiting to fill up, gas rationing in some states, and the federally mandated 55 mph speed limit.

Because domestic crude oil price controls continued in one form or another through to the Reagan administration, the U.S. became increasingly dependent on foreign supplies offset only by Alaskan oil that was not subject to either price controls or the Crude Oil Windfall Profit Tax Act of 1980.

The second major policy shift occurred in 2015, when Congress ended its 1974 ban on crude oil exports. This was the boom period in fracking, and so much lighter crude oils were pumped out of the ground that the supplies overwhelmed the ability of domestic refineries to process the lighter oils.

Other refineries were configured to process the heavier oils imported from Canada, Venezuela, Saudi Arabia and Mexico, and lifting the export ban removed any profit motive for these heavy oil refineries to retool. Today, the U.S. still imports 6 million-plus barrels of heavy crude, about one-third of overall demand.

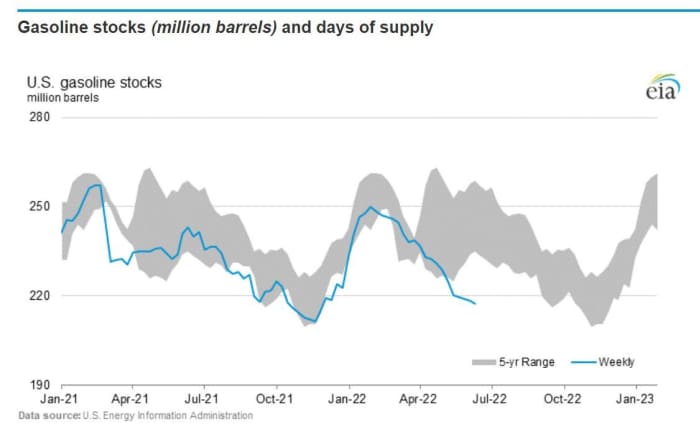

Fast forward to 2022. With the outbreak of the Ukraine war and sanctions on Russian hydrocarbons, there’s more demand for oil-related products from the U.S. Europe is replacing Russian supply with purchases from the global market. The U.S. is one source of those sales, and this would not have been possible had the export ban remained in place. As a result, U.S. inventories of refined products and crude are below five-year averages.

U.S. Energy Information Administration

The third major policy shift was the pullout from Afghanistan, thereby ending the “blood for oil” trade begun by President George W. Bush with the invasion of Iraq and continued through President Trump. Former Federal Reserve Chairman Alan Greenspan in his book “The Age of Turbulence” stated: “I am saddened that it is politically inconvenient to acknowledge what everyone knows: the Iraq war is largely about oil.” President Biden doesn’t have the military in the Middle East, protecting Saudi Arabia, as a bargaining chip for lower oil prices.

The math doesn’t work for refineries to expand

As Biden correctly points out, refinery capacity in the U.S. has dropped. Several have closed in recent years simply because of high operating costs, conversion to renewable fuels, (e.g. Bakersfield, Calif., one in San Francisco, several in the mid-continent, are underway now) mounting environmental restrictions, and damage from hurricanes. One exploded. Some have been on the market for years with no buyers because of low margins and large environmental liabilities.

| U.S. refinery closures | Capacity, barrels per day | Date | Reason |

| PES, Philadelphia, PA | 335,000 | June 2019 | Explosion; bankruptcy |

| HollyFrontier Cheyenne, WY | 52,000 | June 2020 | Conversion to renewable fuels |

| Calcasieu Refining, Lake Charles, LA | 135,500 | August 2020 | Low demand |

| Marathon Petroleum, Martinez, CA | 161,000 | August 2020 | Conversion to renewable fuels |

| Marathon Petroleum, Gallup, NM | 27,000 | August 2020 | Low demand |

| Shell Convent, St. James, LA | 240,000 | November 2020 | Unprofitable |

| PBF Energy, Paulsboro, NJ | 180,000 | November 2020 | Low demand; partial operations |

| Limetree Bay, St. Croix, USVI | 210,000 | May 2021 | Unprofitable |

| Phillips 66 Alliance, Belle Chase, LA | 255,000 | November 2021 | Storm damage |

| Phillips 66 Rodeo, California | 120,200 | May 2022 | Conversion to renewable fuels |

| LyondellBasell, Houston, TX | 263,776 | April 2022 | Close on or before 12/23 |

| Source: Laura Sanicola (Reuters) and company announcements |

That’s before taking into account the push for renewable fuels and electric cars. Profit margins are a minuscule 1.5%, and a greenfield refinery can take five years – if all goes smoothly – and more than $20,000 per barrel of capacity to build. Exxon Mobil is three years into a reported $1.5 billion, 250,000-barrels-per-day expansion at its Beaumont, Texas, refinery.

The payout for building new refineries or expansions is too uncertain in the long run, especially for companies like Marathon Petroleum

MPC,

Valero

VLO,

and Phillips 66

PSX,

that only are in the refining business. Notably, all three have announced renewable fuels ventures.

But before oil can get to the refinery, it must be found and produced. There again, the industry hasn’t fully recovered from the pandemic. Baker Hughes reports that the U.S. rig count, the barometer for drilling, has increased this year by 270 to 740, but below the pre-pandemic number of 794 of January 2020. On top of that, well costs are up; one that would have cost $9 million to drill five years ago now costs $13 million. Tens of thousands of workers have left the oil patch and are not going back. Together, Trump’s steel tariffs and supply shortages have doubled the cost of tubulars.

It’s not just a U.S. problem. Baker Hughes reports that the Middle East rig count is at 817, still down more than 25% from pre-pandemic level of 1,104. Middle East wells are much more productive than the U.S. shale wells and, lest we forget, the reason that OPEC could wage an extended price war against the U.S. producers a decade ago that pushed oil below $40 a barrel in 2014.

The Middle East was hit hard by the global pandemic shutdown. Revenue plummeted. It is a fiction that OPEC nations have excess supply to deliver to the world market. At these prices, EVERYONE should be producing.

Reports are that Russian crude oil production has dropped since U.S. and European oil companies and oilfield service companies have exited the country. At the same time, Russia’s military needs more oil for the war in Ukraine. These two actions combine to reduce the net supply available to the world market and place further upward pressure on price.

European nations are unlikely to re-embrace Russia’s hydrocarbon supplies after the war. Because it will take some number of years for Europe to adjust completely, the U.S. will continue to sell more refined products and oil to Europe. U.S. consumers are bidding for gasoline against buyers in Berlin.

Biden’s frustration is evident. He continues to release 1.0 million barrels per day from the nation’s Strategic Petroleum Reserve, but the impact on price has been minimal. Some goes overseas as Americans subsidize fuel prices across the world. The stockpile is limited, and in this competitive game, OPEC has more staying power.

The bottom line is there are no quick fixes for Biden or Congress. Short-term policy actions in the name of midterm elections and expediency will fail to help consumers. A recession could stop an overheated U.S. economy to drive down demand for gasoline, but the political costs would be even higher.

Anyone who claims to have a fix is just playing politics.

Ed Hirs is the managing director of Hillhouse Resources LLC, an independent E&P company working onshore conventional oil and gas along the Texas coast as well as an inaugural University of Houston Energy Fellow.